Investing in VonZu Tech - a memo to myself

Globalisation and Retail

Have you ever noticed that in the list of the richest people in every country there is always at least one Retail family? This is true in the US (e.g Walton family), Germany (e.g. Albrecht family), in smaller countries like Portugal (Soares dos Santos family) and is the same even in China (Ma family, Colin Huang).

There is a reason for this: retail goods and food is one of the highest spend categories of households in any country.

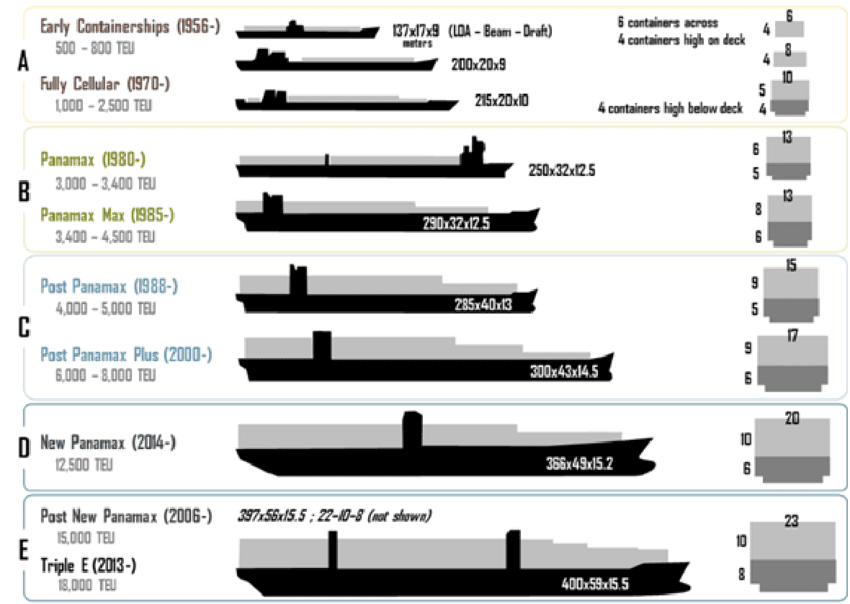

The last massive transformation that made the money of many of this families was an invention from the 1960s: the sea container.

The evolution of retail via mega chains and stores with their professional category managers and international sourcing teams was made possible by this pice of logistics infrastructure. And this was very much what led to the massive expansion of global trade from 1960 to 2019.

My hands-on experience with global trade was first gained as CEO of Spiriant GmbH in Germany, a company that sourced the airline cabin equipment for major airlines worldwide. Spiriant sourced for each of its airline customers about 2,000 items including glasses, blankets and amenity kits. In the 2005, Spierant went through a similar evolution as other much bigger retails and wholesale companies: direct sourcing. We went from working with European brokers to connecting directly with trading houses in Hong Kong and later going directly to contract manufacturers in China, Vietnam etc.

I remember well when my team took me to visit Li & Fung, a 12 Billion USD trading house in Hong Kong. We toured their private B2B shopping mall, which many procurement teams of retailers around the world know well. They served essentially as a bridge between factories in mainland China and the retailer sourcing teams. They allowed us to to be much more effective than using European trading houses. But the truth is that a few months later we were scouting ourselves for factories and contracting directly to manufacture the items we engineered.

I was soon being taken by my team to visit the factories in mainland China. These trips to Shenzhen and other locations were even more amazing: we would drive kms through roads with factories in either side of the road.

This was the journey that all major retailers in the western world went through. Our office in Kowloon was in the same building of many other sourcing teams.

The impact of this evolution is mirrored in the evolution of the container fleet from 1960 to today:

The Retail Supply Chain

The Retail models we know today (like shopping malls, hypermarkets, etc) are a result of this transformations in supply chains. They replaced the many layers of wholesales and small retail chains and led to the gentrification of small local stores. It was just impossible to compete with the scale of the companies that mastered these massive supply chains and the global trade game.

Consolidated orders are transported in full container loads to distribution centers (DC's) closer to the markets. In the DCs items (SKUs or Stock keeping unites) coming from all suppliers would be consolidated and distributed to the supermarkets.

I visited many of this operations later during my work at Kuehne + Nagel, one of the biggest logistics companies in the world. I was amazed by the cross-dock platforms for food retailers where the daily deliveries to thousands of fresh, ambient and frozen items would get prepared for delivery or platforms for all sorts of other goods like electronics or pharmaceutical products.

The cadence of these platforms is dictated by the arrival of the orders from stores to replenish their stock levels and shelves. The stocks at the shop served as a first buffer for variability in demand from individual customers, while the stock at DCs would buffer overall fluctuations.

As customers, we stroll the supermarkets and shops in the shopping malls buying something here and something there, while in the background, similar to a gigantic Swiss watch, all is being orchestrated by the supply chain managers.

The new retail

Fast forward to today. I just ordered a net to protect my balcony from birds directly from a factory in China through Wish for 8 USD. It will be packed for me and sent to my place in Portugal. No traders, no travels to HKG, no shops, no supermarkets. This is a part of a massive transformation in retail. The internet is massively changing the way we buy. It started with companies like eBay and Amazon but it is now every where. Welcome to the new world of retail!

We are being perfectly "conditioned" to this new way of buying: we seat in our sofas and stroll down this massive amount of choice in our phones. With a single click we order whatever you need from anywhere in the world. All will be packed and delivered to our homes. And if we don't like it, we send it back.

At first the upstream processes of these logistics chains did not change: orders from the factories would arrive in full container loads at DCs. But there was a massive change in the downstream: instead of a single multi-item truck load deliver to each stores every day, goods are commissioned according to the order of the final customer and sent to their homes directly. There is no more stock buffers in shelves.

Orders came in real time and "packing" became a much more important process.

The last mile delivery became much more similar to the parcel business. It is therefore no wonder that major parcel companies become the main rails for eCommerce. These were companies that were created for point to point deliveries from the outset. Actually the origin of their business model is also connected with the invention of containers, but that is material for another story.

But things started to change in the last five years: Amazon, started being sceptical about last mile distribution costs and making first attempts to create alternatives to the integrators (the DHL, UPS etc of the world).

The future Retail Supply Chains

The thinking is quite simple: when an online retailer tenders the last mile delivery for say 10 million yearly deliveries in Spain per year, it will receive a price that might go from 3€ to 5€ per delivered package. Each logistics operator will try to find the most effective way to deliver this volume, but it will certainly need to take the volume variance risk into account, as this is something that they don't control. Once the team of this retailer does the sourcing game two or three times, it will probably have exhausted the maximum potential of playing the integrators against each other in a bidding process.

Another major pain problem, is the impact of Amazon prime and some day deliveries. eCommerce companies are conditioning consumers to the expectation of same day deliveries. Logistics networks of the past don't accommodate this easily. Distribution networks and integrators hub and spoke models are designed for a world operating in a day one order to day three delivery cycle.

The impact of these two trends on the logistics infrastructure is huge. Best in class retailers are building networks of last mile delivery operations with many operators, a mesh of multiple solutions. They include central warehouses, the commissioning of goods in third party warehouses, smaller warehouses inside cities, dark warehouses inside the neighbourhoods and pop-up storing facilities. The Supply Chain of the future is much less organised and requires technology to deliver its promise.

Logistics Tech transformation

The transformation of this new models in Retail is dramatical. The trade flows with containers full of pallets of a single product are giving space to containers full of orders of multiple customers. The location and footprint of distribution centers is changing.

But one element is remarkably stable: the last mile delivery of what you want into your door step. The main transformation is on who is in the best position to deliver the productivity that makes this form of delivery profitable to retailers, logistics operators and individual drivers.

Applying first principles to this problem implies that the lowest cost comes from those operations that get the best use of the person climbing stairs and walking the streets to deliver your orders. Increasing the average deliveries per hour is a win-win for all involved. Amazon was the first to understand this. Instead of contracting a price per package by big operators it started contracting with small 3Pls and 2PLs and delivery service paid by flow. That is, a payment for the capacity to deliver independently of the number of packages to deliver.

This new approach separates the transport service (which the 2PL and 3Pl can control) from the risk of the retailer business (the number of packages to deliver). It makes the optimisation of the last mile productivity an endogenous variable of the retailer business and another parameter for the machine learning optimisation models of marketing of the retailer.

Enter VonZu Tech

A true win, win win.

- The change in retail described above is not only true in traditional non-food retail. It is true in food, food service and many of the new services enabled by digital-first. Vonzu proves that the supply chain challenges of managing a fleet of scooters is the same of managing the last mile delivery of goods (Acciona is a customer of VonZu to manage its mobility services)

- In the dynamic & complex reality of retail, it impossible for a single solution by single company to cover all the needs e.g. SAP or Oracle. It is about collaboration across multiple agents in a dynamic and autonomous way. Focusing on the how and where that orchestration will take place is where companies like VonZu Tech can prosper

We continue to look for teams working on this transformation. The upstream part of the industry will need to adapt to the changes of the realties of commerce. Thinking about the transformation from the factory to the home is wrong. As the principles of lean manufacturing teach us, you should start at the home to look at new way of doing business and work then upstream to see how logistics will change e.g. the forwarding industry. The new rails of commerce will allow a new form of "small" retailers. They are not the neighbourhood shop as we used to now it but more similar to mini Li and Fong's. They connect digital manufacturers to clients by being eCommerce first companies.

Comments

Post a Comment